2021 Q4 Review and Outlook – The Most Hated Bull Market in History

2021 charged across the finish line as the S&P 500 SPDR ETF (SPY) gained 11.1% in the fourth quarter. The U.S. bond market (as measured by the US Aggregate Bond ETF – AGG) was down slightly (-0.1% return), and a 60% stock/40% bond portfolio gained 6.6%.

Again, that was just the fourth quarter. For the full year 2021, the SPY returned 28.4%, bonds lost 1.8%, and a 60/40 portfolio gained 16.5%. This is the third consecutive year that the S&P 500 returned over 15%, which almost makes you forget how crazy the last three years have been.

The last ten years were also impressive, with the SPY returning 16.5%/year, bonds returning 2.8%/year and a 60/40 portfolio returning 11.1%/year. Furthermore, both the SPY and a 60/40 portfolio recorded only one negative year during this period (2018: -4.6% for SPY and -2.6% for 60/40, respectively)

Figure 1: S&P 500 quarterly performance, trailing four quarters.

Source: Strategas

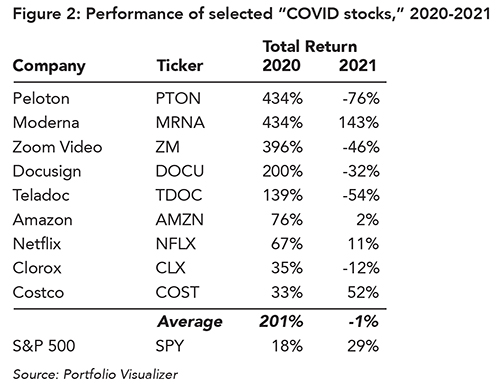

Chasing the COVID stocks didn’t work out very well.

Quick quiz – what were the three highest performing stocks in the S&P 500 in 2021?

Answer: Devon Energy (DVN) was #1, Marathon Oil (MRO) was #2 and Fortinet (FTNT) was #3. There is close to a 0% chance that in January 2021 anyone expected any of these three stocks to be the top three of 2021.

When COVID hit in early 2020, most stocks fell off a cliff – except for a few companies which benefited from some combination of quarantines/vaccines/toilet paper/boredom. Those companies (some which were not yet profitable) took off like rockets as speculators chased the trend. We hope that these investors sold before 2021 rolled around, because, for the most part, the rockets ran out of fuel and turned into rocks. The following table shows a selection of the hottest COVID stocks of 2020, and how they did in 2021.

While not all these rockets fell back to earth, they woefully underperformed the S&P 500 on average in 2021, with only two stocks (Moderna and Costco) outperforming on an individual basis. Also, while Moderna returned 143% in 2021, it is down more than 50% from its 2021 peak.

Furthermore, we would argue the “COVID theme” is still here in 2021. The world still looks more like it did in 2020 than 2019, with increased remote work, sporadic shutdowns and shortages of essentials. This would imply that the COVID stocks should still be growing like Jack’s beanstalk. Apparently, they didn’t get the memo (or Zoom invite, as it were).

Trying to time the hot trend is a dangerous game and is no different from betting on your favorite team to win the Super Bowl. Is it fun? Yes! Exciting? Yes! Profitable? Sustainable over years and decades of investing? Anyone? Bueller?

What to look for in 2022

As we continue our journey through the Greek alphabet in 2022, there are a few things we are keeping our eye on. This doesn’t mean that we are going to try and make our portfolios zig and zag with every Fed pronouncement or news story, but it helps to understand where the world sits from an economic and political perspective.

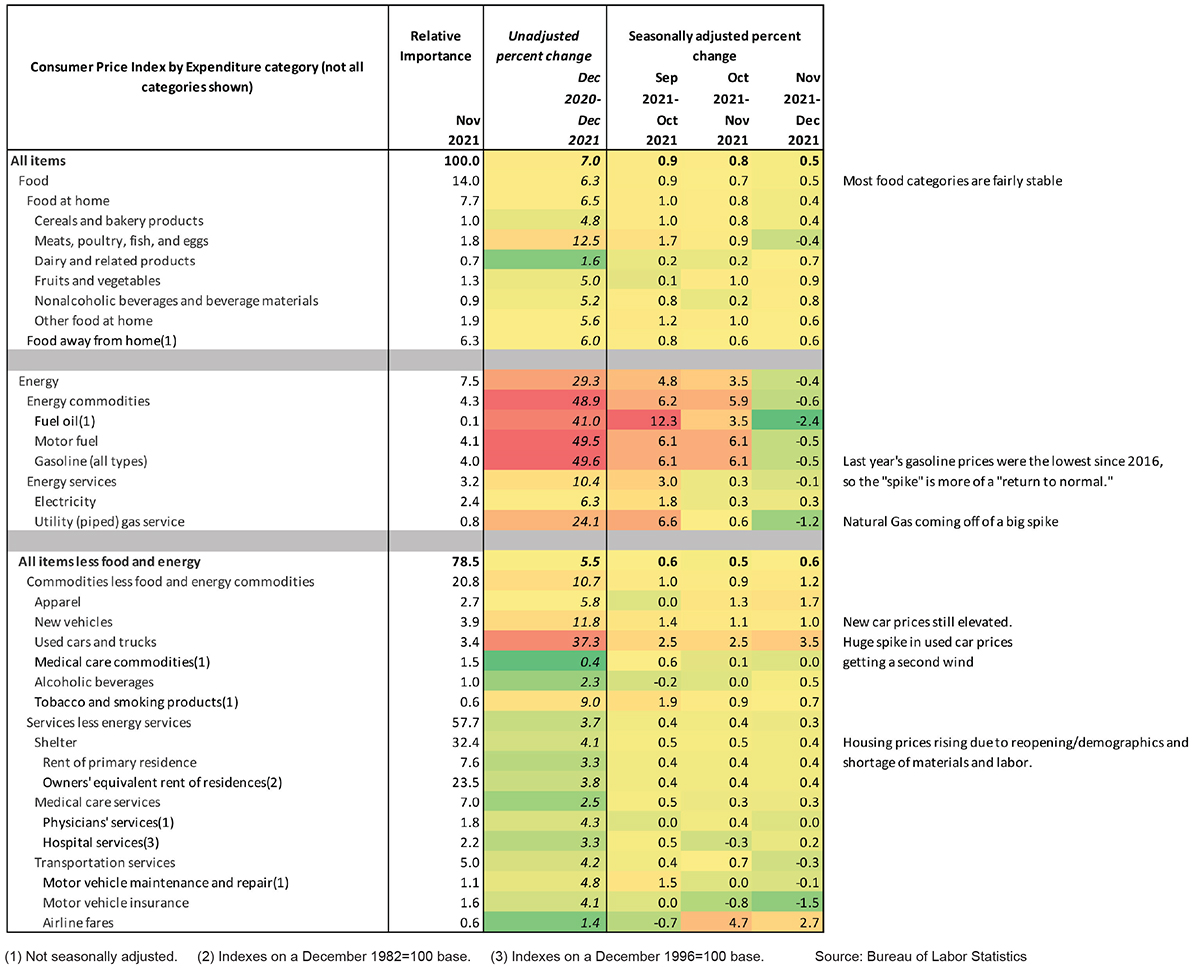

Inflation – We will probably be following inflation for a while, because it will be with us for a while. Figure 3 provides the latest numbers, and they look a lot

like the data from three and six months ago – a big spike in energy and auto prices combined with higher prices on almost every other category. While we have written in past updates that a lot of the triggers for high prices are somewhat “transitory” (an overused and misunderstood term), that doesn’t mean everything magically snaps back into place in six months. Plus, more “structural” changes (e.g., higher wages) are creeping into the equation, which will probably cause the long-term inflation rate to settle higher than the 2% we enjoyed over the past ten years or so, which itself was a historical anomaly.

As we have written before, stocks can be a great long-term inflation hedge, as companies can pass along their higher costs to the end consumer. While a lot of companies’ margins are currently getting squeezed as they eat the higher costs in the short term, that eventually corrects itself. Plus, energy and materials stocks have done very well over the past 12 months and should book outsized profits as oil and commodity prices stay high.

Federal Reserve actions – One byproduct of changes in inflation is in the behavior of the Federal Reserve. For a long time, they could afford to be very stimulative with monetary policy and keep both short and long-term interest rates low in order to maximize economic growth. It is increasingly clear that Chairman Jerome Powell intends to tighten things up, which would imply an increase to interest rates across the board.

In our view, the immediate effect of interest rate increases is bearish to stocks (especially growth stocks with low or zero dividends), as higher interest rates reduce the value of future growth – a stock with a 1% dividend yield that is growing at 10% per year looks good if you are only getting 1.5% on a 10-year treasury bond (which grows 0% per year), but the picture starts to get cloudier at a 3% treasury bond yield, and the stock price may have to adjust to compensate.

However, stocks ultimately grow at the rate of profit growth, and a healthy economy (which the Fed is trying to cultivate) should provide enough fuel to feed that profit growth which will hopefully compensate for the possible pain of short-run volatility in stock prices with solid long-term returns.

One risk is that the Fed over-reacts and triggers a recession, although we think that Powell & Co. is leaning on the side of not triggering a recession while accepting a slightly higher than “ideal” long-term inflation rate. Another risk is that the economy doesn’t respond to Fed actions in the way that investors (or the Fed itself) expect, which damages the credibility of the Fed and stirs discontent in the markets – which would cause a lot of volatility. Whatever the case, it’s hard to see how this will ultimately play out, especially over the next 6-12 months.

Pace of Reopening/Supply Chain –There are still several factors that are pulling against each other in the extremely complicated global supply chain. Container ships full of cargo are still backed up at ports, chip fabs are slowly coming back online but are not yet 100%, trucking companies don’t have any drivers and so on. And, solving one issue is sometimes dependent on solving another one (which may not want to be solved just yet.)

On the demand side, the re-opening is now a “re-re-opening” as Omicron has caused more disruptions. However, the effects don’t seem to be nearly as severe as the original wave or the Delta wave, as a) vaccine penetration is much higher than before, and b) a lot of people have simply accepted COVID as yet another disease to be dealt with. Something that was a pandemic is now “endemic,” and the economy is adapting accordingly.

Putting the two together, we still have a healthy economy that is lurching forward in fits and starts as supply chain snarls and the occasional lockdown occasionally interrupt what seems to be steady forward progress. While the recessionary risks are still out there, the current trajectory is still positive.

“Surely this is the top/this cannot persist/we are in a bubble.”

The cloud attached to the silver lining of historically strong stock market returns is the increasing stress level some investors experience as the market plows higher and stocks become more expensive.

Adding to the stress is a highly vocal population of doomsayers who believe the END IS NEAR. In fact, the period from 2009 to the present has been termed by some as the “most hated bull market in history,” as people confuse the non-stop drip-feed of ominous reports on the nightly and/or financial news (which gets more viewers than “boring” in-depth analysis) with the impending crash of the stock market.

To be fair, there was that frightening stock market crash in early 2020 when investors saw the potential economic devastation that COVID could (and did) bring upon the world, and the top to bottom drop of the SPY was a little more than 30% over the span of a month. This was a stressful time to be in the investment business! However, the stock market looked ahead to a strong recovery – seemingly before anyone else did – and all that lost ground was made up by August, and the S&P 500 finished the year up over 18%.

The recovery was so strong that people (especially ones who talk loudly on CNBC) are now worrying that it is too strong, based on the current inflation numbers. No good deed goes unpunished.

We came across a quote from The Bahnsen Group that does a great job of putting into words our view of the last 10 years: “There have now been 343 record highs since 2013. That is 343 times someone could have said ‘I don’t want to invest at an all-time high’ and been wrong. 343 times that markets have confounded the silliest mathematical argument imaginable.1”

Now, we are not ignoring the possible future risks for the economy and/or stocks. Stocks do have stretched valuations, as the price you pay for a dollar of profits has risen more quickly than the growth in profits. Inflation does have a corrosive short-term effect on company profits, as they can often struggle to initially pass on their higher costs to consumers. As we noted in the previous section, the Federal Reserve is also increasingly worried about inflation, which may cause Mr. Powell to take actions to cool the economy down that could reduce economic growth.

However, instead of trying to predict the next big crash or forecast this year’s S&P 500 return, we take a longer view and acknowledge that average long-term (i.e., 10+ year) returns are a) definitely going to be lower than the last three years’ blistering performance; b) most likely going to be lower than the previous 10 years; and c) probably going to be lower than average returns over the last 50 years.

The dividend yield on the S&P 500 is about 1.3%, and the expected long-term economic growth is probably going to be around 2% per year after inflation, which means that “real” (i.e., after inflation) long-term stock returns will probably be somewhere close to 1.3% + 2% = 3.3%, which is lower than the historical average of 5%-6% per year. Adding 2.5%-3.5% inflation gives you 5.8%-6.8% future total returns (which is lower than the historical 9%-10% annual returns). This is still higher than the 1.5%-2.5% expected return on investment-grade corporate bonds, although the risk is also higher.

We take this longer-term view of stock returns, because stocks are meant to be held for a long time. If you are taking large withdrawals from your investment portfolio (or anticipate a need for large withdrawals in the near future), then you shouldn’t have all your portfolio in stocks. This is why we recommend clients include at least some bond allocation to their portfolios – despite the low yields. A bond allocation can help cushion the inevitable crashes and provide “dry powder” to rebalance into stocks when they are down.

A well thought out financial plan can also bring some peace of mind, as it helps you focus on long-term goals rather than short-term market fluctuations. If you would like help creating or updating a financial plan, please contact us.

_________________________________________________

1 “DC Today,” David Bahnsen, thebahnsengroup.com

Figure 3: Selected Components of the Consumer Price Index (CPI), December 2021