2026 Q1 Review and Outlook – Bombs, Blockades and A.I.

2026 Q1 Review and Outlook – Bombs, Blockades and A.I.

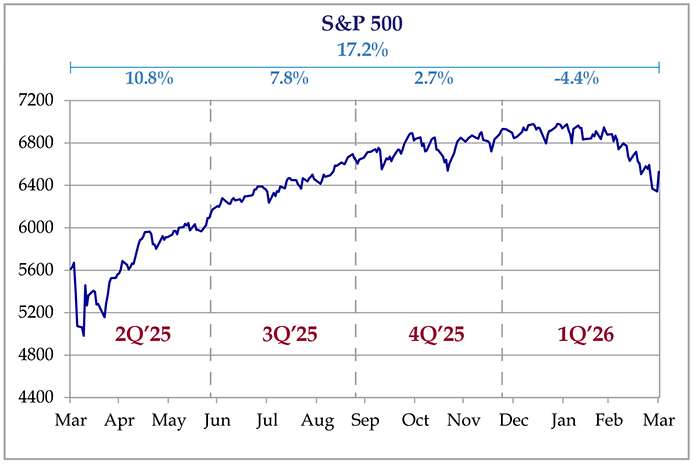

The market stumbled out of the gate in the first quarter of 2026 as stocks (as measured by the S&P 500 SPDR ETF – SPY) declined by 4.4%. The U.S. bond market (as measured by the US Aggregate Bond ETF – AGG) was flat, and a 60% stock/40% bond portfolio earned negative 3.7% total return.

Figure 1: S&P 500 quarterly performance, trailing four quarters.

Strategas, Portfolio Visualizer

Bombs, blockades and other low-stress activities

Just a month before the anniversary of last year’s “tariff tantrum”, chaos descended on the world as the U.S. and Israel commenced a bombing campaign in Iran on the last day of February. In response, Iran fired back with drone and missile attacks on Gulf state oil facilities and U.S. military bases in the region. In addition, Iran clamped down on sea traffic through the Strait of Hormuz, which just so happens to transport about 20% of the world’s oil. While there was a cease fire declared on April 7th, the peace is fragile, and the Strait is far from open, as Iran’s blockade has been countered by a U.S.-led blockade of Iran’s ports. We can only imagine what it’s like to be a tanker captain enroute to or from the Persian Gulf.

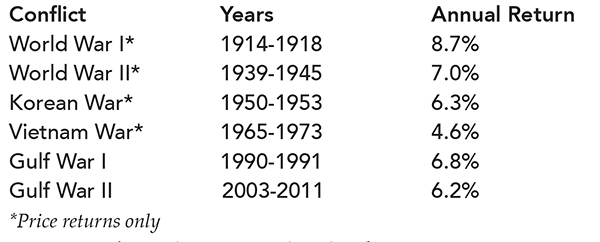

The chaos predictably upset the global investment community, and stocks fell almost 10% before charging back to new highs post-ceasefire. However, it’s not necessarily the war itself that shook the stock market. Wars are horrible events which cause widespread destruction and loss of life. However, the stock market is pretty good at looking past the war and most wars have resulted in gains for U.S. stocks. It helps that the U.S. has been physically insulated from the worst effects of war, which can completely erase the economies and stock markets of “battleground countries” such as Germany or Russia. (Russia’s stocks are still untradeable as a result of sanctions from the ongoing war in Ukraine). Figure 2 shows a summary of the major U.S.-involved armed conflicts and the resulting stock market performance:

Figure 2: U.S. Stock Market Performance – Historic Armed Conflicts

Source: Davidmanuel.com via Copilot, Bloomberg, Factset

Other factors that influenced returns:

- While most of the wars were “profitable,” there were some steep drawdowns, particularly at the outset.

- Due to high inflation (especially during the Vietnam War), “real” returns were much lower.

- The return from Gulf War II included the Great Financial Crisis of 2008-2009, which had very little to do with our troops fighting in Iraq.

- The U.S. was in the middle of a recession during Gulf War I.

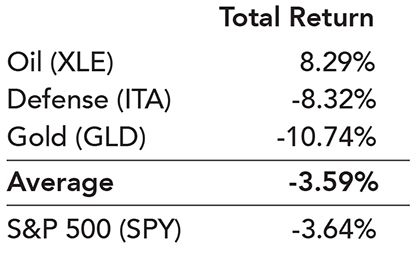

But surely we can make some “easy money” trading the initial shock of the war, right? After all, “everybody knows” that, if there is a war in the Middle East, you buy oil stocks, defense stocks and gold. Maybe…maybe not. Figure 3 shows the result of making the “obvious” war trades from the first bomb dropping on February 28th to the ceasefire announcement on April 7th.

Figure 3: Epic Fury Trades: 2/28/2026 to 4/7/2026

Source: Koyfin Financial

All that effort just to match the S&P 500’s 3.6% decline. While defense stocks may benefit from the massive restocking of equipment that was expended or destroyed in the conflict, the stocks were already on the rise before the conflict. Likewise, gold fell like a shiny, dense rock from extremely high levels. Oil stocks were the only successful trade although performance had been stagnant for several years leading up to the conflict.

The lesson here isn’t to ignore what is happening. It’s more to realize that financial markets are very good at quickly absorbing information and looking past what is already in the news.

Software ate the world – and A.I. is eating software

Although we talk about “the stock market,” there is always more going on under the surface – and sometimes a “diversified” portfolio is less diversified than you think.

In 2011 (which was 15 years ago if you want to feel old), technology entrepreneur and venture capitalist Marc Andreessen wrote a famous essay titled Software is Eating the World, Mr. Andreessen (who founded Netscape, the maker of the first web browser) wrote “…we are in the middle of a dramatic and broad technological and economic shift in which software companies are poised to take over large swathes of the economy.” Although he didn’t quantify his prediction, it was correct in spirit, as companies such as Microsoft, Apple and Amazon (which is now more of a cloud services provider than an online retailer) had massive gains in value. If you simply read the article, went “huh, that’s interesting,” and put $10,000 into Microsoft, you now have about $250,000.

“Software as a Service” (SAAS) companies popped up like daisies and grew revenues at an astounding rate by plugging into Corporate America. Almost every major company now does business with Salesforce.com (customer management), Workday (HR), ServiceNow (back office), Zoom (communications), etc. Investors loved the subscription-based revenue model and low capital requirements – just some office space and some smart and hard-working programmers.

Within the last three months, however, the software industry got a rude introduction to the term “creative destruction.” In February, Citrini Research wrote an article titled The 2028 Global Intelligence Crisis, which presents a hypothetical situation in 2028 when Artificial Intelligence gets smart enough to (in theory) replicate a lot of what software companies do at a fraction of the cost. It paints a grim picture, opening with “The unemployment rate printed 10.2% this morning [in 2028], a 0.3% upside surprise.”

Further down the page was the paragraph that sent tech investors into a panic.

“A competent developer working with Claude Code or Codex could now replicate the core functionality of a mid-market SaaS product in weeks. Not perfectly or with every edge case handled, but well enough that the CIO reviewing a $500k annual renewal started asking the question ‘what if we just built this ourselves?’”

Software stocks immediately dropped like a rock, and it didn’t stop there. If A.I. can write my business’s software, why am I paying for an expensive consulting company to tell me what software I need? Why am I paying so much for payroll services like Paychex and ADP? And who needs payroll companies if you fire everybody except the CEO and his/her “A.I. whisperer?”

And it kept going. The “alternative asset managers” – particularly “private credit” managers – managed funds that had a large portion of assets invested in…software companies. (As much as 25% to 30% of some funds). The contagion spread to the alternative asset manager stocks, sending them down 20% to 30% in only 3 months.

A lot of institutional and high net worth investors felt that investing in private funds would insulate them from volatility, since the funds don’t mark their holdings to market. However, it’s amazing what happens when you want to make a withdrawal at the published “Net Asset Value” (NAV) and the manager only gives you 10% of what you ask for because the fund is full of loans to software companies and the manager is trying to keep the flood of panicked investors from forcing sales of those loans (at what is probably less than NAV). The market price is eventually discovered – sometimes at the worst possible moment.

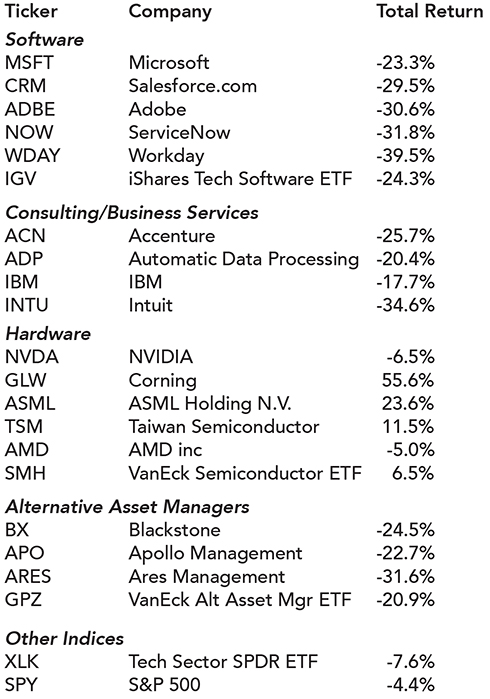

Figure 4 summarizes the carnage from the A.I. threat in the first quarter, along with a few A.I. beneficiaries – mainly hardware companies.

Figure 4: 1Q2026 returns for selected A.I. targets and A.I. beneficiaries

Source: Koyfin Financial

If nothing else, this teaches an important lesson in diversification. If you say, “I’m invested in tech,” what kind of tech? Corning (up 56%) or Workday (down 40%)? Or, “I don’t own those volatile tech stocks – I own financial stocks.” That depends on which financial stocks.

Now, you might think “great, I’ll just sell (or don’t buy) everything on this list that’s down since the market is always right.” It’s not that simple. The market often overreacts, and we believe that some of the pronouncements (especially by CEOs of A.I. companies) are far-fetched. However, sometimes the market underreacts, and, for some companies, this is the first signal of a long and painful decline. You must sift through the overwhelming amount of information on both sides and try to figure out what’s pie in the sky vs. a sustainable trend. In fact, most of the “losers” on the previous table had a nice pop upward in April, as the software ETF (IGV) increased 6% in only two weeks and Blackstone (BX) is up 12%.

Again, the key lesson here is the importance of true diversification. Owning broad market indices such as the S&P 500 or All-Country World Index will certainly meet this requirement. If you are into stock-picking or even sector-picking, you need to make sure there aren’t hidden imbalances or concentrations in your portfolio. We certainly strive to own a “little of everything” — we own some of these losers, but also a few of the big winners and they all have strong management teams that can hopefully adapt their company to take advantage of these trends. However, we are certainly going back over the losers list with a fine-tooth comb, sifting the “overreactions” from the “long painful declines.”

Inflation is back in the news

As we imply in the first section, the greatest angst surrounding the Iranian conflict is oil prices. With 20% of the global oil supply bottled up in the Persian Gulf, oil prices skyrocketed, and now we are seeing $4 per gallon gas. While the U.S. car fleet is much more fuel efficient than 20 or even 10 years ago, sharply rising gas prices still have a psychological impact on consumers.

The initial effect of the closure of the Strait of Hormuz hit the latest CPI report as rising energy costs contributed 0.8 percentage points to a 3.3% March inflation rate. That’s almost a quarter of the total number. The timing especially hurts, because the “Core” inflation rate came in at a lower than expected 2.8%. Just as we are starting to get things under control (and give the Fed more room to cut rates) oil ruins the party.

Interest rates – which are very sensitive to future inflation expectations – jumped across the board, which in turn increased the price of mortgages and car loans. In fact, the average 30-year fixed mortgage rate jumped from just under 6.0% at the beginning of March to almost 6.5% at the beginning of April. Assuming there is no near-term relief for oil prices, economic activity could slow, although we don’t believe it will lead to an outright recession (more on that in the next section).

While that sounds a bit downbeat, remember that the situation can change on a dime. In fact, during the last week, gasoline futures prices dropped as much as $0.30 per gallon on news that the talks/blockades/bombings appear to be going in the right direction and stocks pushed back to all-time high levels.

The Economy provides some wiggle room

Despite the disappointing oil-fueled inflation news, U.S. economic indicators continue to hold up surprisingly well considering the sluggish housing market and an unemployment rate that crept upward in 2025.

- GDP growth continues to hover around the 2% mark, which is “solid but not spectacular,” and far from recession territory.

- The Coincident Economic Activity Index (i.e., what is happening “right now” in the economy) finished 2025 with strong upward momentum.

- The Leading Index (i.e., the forecast of the Coincident Index six months from now) made a healthy jump from January to February, hitting an 8-year high.

- The unemployment rate is bouncing between 4.3% and 4.5%, with March’s number down from February.

- S&P 500 earnings grew at a double-digit percentage rate for the sixth consecutive quarter.

This provides the economy with a cushion to absorb the oil price shock (as long as oil prices don’t stay high for an extended period) and the current rally in the stock market to new highs implies that the “Hormuz premium” on oil will be resolved sooner rather than later.

If you could take anything away from the current chaos it is “stocks are long-term assets” which are not designed to pay for short-term expenses. We fully expect more of these dips (and worse) several times over the next 10-20 years – we just don’t know when they will occur. That is the “nature of the beast.” As usual, if you have a sound financial plan and have a high quality, diversified portfolio you should be able to ride out the inevitable war, blockades, A.I. apocalypse and other “low stress stuff” that the world can and will throw at you.

Enjoy the warm Spring weather and we will be back with Summer and fireworks in July. Please contact us if you have any questions.