2025 Q3 Review and Outlook – Bubble, Bubble, Toil and Trouble

The market continued its upward swing in the third quarter of 2025 as stocks (as measured by the S&P 500 SPDR ETF – SPY) rose 7.8%. The U.S. bond market (as measured by the US Aggregate Bond ETF – AGG) gained 2.1%, and a 60% stock/40% bond portfolio earned a 5.5% total return. Year to Date (YTD), stocks gained 14.4%, bonds gained 5.8% and a 60/40 portfolio gained 10.9%

Figure 1: S&P 500 quarterly performance, trailing four quarters.

Are we in an AI bubble?

In case anyone hasn’t noticed, the stock market has been on a tear since the end of 2022. In fact, almost every stock market in the world is in a bull market. The terrible performance of both the stock and bond markets in 2022 seems like a distant memory. To paraphrase the Black Knight in Monty Python’s Search for the Holy Grail, 2022 was “just a flesh wound!”

An ever-rising stock market makes just about everybody happy. Even people who don’t have a lot invested get a pep in their step seeing the good news (for a change) from CNBC and Yahoo Finance. However, as the resident grumpy bean-counting curmudgeons, we are starting to get a little bit concerned about the type and level of discourse about the market, particularly in “technology land” and especially in “AI land.”

Normally, we don’t get involved in short-term discussions about market behavior – you will never hear us say “this is the top” or “this is the bottom.” We operate with the understanding that the stock market is a random number generator over short (i.e., less than 3-5 years) timeframes, but it reliably follows economic growth over timeframes measured in decades – which is the appropriate time frame to measure stock returns.

And yet…

We are well aware of what’s happening around us, and most of us at TCV (being of a certain age) have the scars from bubbly times in the past, so we tend to sit up and pay attention when stocks like Oracle (ORCL) jump 20% in one day just from an announcement of a partnership with an unprofitable AI company. Or when AMD spikes a similar amount from a similar type of announcement. Now, companies make announcements about partnerships with other companies all the time. However, we were taken aback by a) the massive numbers involved; b) the long time frame to completion; and c) no mention of how anyone is going to pay for these deals.

In Oracle’s case, Open AI doesn’t currently have nearly enough money to pay for the $300 billion of servers they are hypothetically ordering from Oracle and Oracle doesn’t currently have the money to build the servers mentioned in the deal. In AMD’s case, the AI company is reportedly paying AMD largely in stock for its future hardware purchases. While the capital markets in the U.S. are the largest, most liquid and most innovative in the world, there is going to be a lot of heavy lifting by investors to scrape the money together. These kind of “funny money” deals are one sign of the dreaded “B word.”

But are we really in an AI bubble? Despite the behavior of the stock market and the dubious partnerships, we may still be a little ways off from the environment that marked the top of the original tech bubble in 1999-2000.

- First, the main players in AI Land are making money and growing profits. NVIDIA, Broadcom, Oracle, Microsoft, etc. are generating massive amounts of cash flow as data centers are popping up like daisies, filled with expensive servers. For example, in 2023, NVIDIA’s generated about $5.6 billion in operating cash flow. Over the past 12 months (i.e. less than two years later) operating cash flow was over $77 billion. That is a massive increase, particularly considering the size of the company. Over the past 5 years, Broadcom has doubled its operating cash flow, from $12 billion to $25 billion. While accounting profits can sometimes be manipulated, cash is cash.

- Second, the rising profits are almost keeping up with the stock prices. Almost. While valuations in the tech sector are quite stretched, we aren’t seeing truly insane valuations, like Cisco Systems trading for 100 times profits at the peak in 2000. NVIDIA is trading for 32x earnings. However, NVIDIA’s profits are expected to grow almost 50% this year and almost 40% next year.

- Finally, while there are an increasing number of market cheerleaders saying the forbidden words “this time is different,” we haven’t seen the extreme type of behavior among the less experienced and/or naive investors. There aren’t widespread reports of people quitting their jobs to trade stocks full-time, and Uber drivers aren’t giving stock tips to mutual fund managers. In the real estate bubble of 2005-2007, cocktail waitresses were buying multiple houses sight unseen to flip to other investors. Right now, there are still pockets of skepticism, and the hyberbolic statements from the AI community are mostly related to how “AI is changing the world” rather than “AI is going to make me filthy rich.” Maybe they are just hiding their greed better than the tech investors in 1999 or real estate speculators in 2006.(Or maybe they are “getting rich quick” in cryptocurrency.)

Nevertheless, we are growing a bit concerned. While the “picks and shovels” companies are making tons of money, the actual AI companies (Open AI, Anthropic, Perplexity, etc.) are not profitable and are not expected to turn a profit for years. If the companies that sell to the end user can’t make money, then the entire sector won’t be able to sustain any growth and investors will lose interest. While there is still a huge runway, with deep-pocketed investors willing to invest in the growth of this supposedly world-changing technology, most of the world-changing companies don’t make it to the finish line. The automobile was one of the most revolutionary technologies in history, but most of the investors’ cash was set on fire, as 200 car companies were whittled down to three in the U.S, with two of the three (GM and Chrysler) going through bankruptcy along the way. Any slowdown in the pace of investment from the AI companies would generate a severe ripple effect across the entire sector, since the stock prices are expecting a continued blistering pace of growth.

Quality Stocks (and other neglected assets)

So what is an investor to do when most of the growth in the market comes from one or two sectors? Well, you could try investing in companies that aren’t directly dependent on AI for its revenues. There are a lot of very profitable companies with attractively priced stocks that will never see the inside of a datacenter. In fact, they may reap some of the benefits of AI without having to make multi-billion-dollar investments.

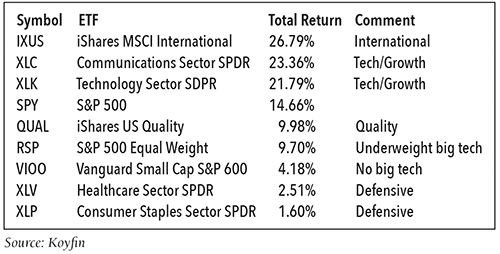

Quality, in the investing sense, has been a bit neglected lately, as have certain “defensive” sectors such as Healthcare and Consumer Staples (both which have many high-quality companies). To be fair, these sectors have their own challenges, such as slowing global growth and rising input costs for staples companies and a tighter leash on government spending for healthcare. However, we believe that a lot of perfectly solid companies have been left behind. The following chart shows various sector ETFs’ year to date returns.

Figure 2: Year to Date Performance to 9/30/2025

Quality stocks have lagged the S&P 500, which has become increasingly weighted toward “big tech.” (NVIDIA alone is now 8% of the S&P 500). The lag becomes more pronounced the further away you get from big tech – even though there are many highly profitable and growing companies in these sectors. As we mentioned in our previous update, international stocks have beaten everybody, although it is mainly due to a) a weakening dollar and b) a rebound from 15 years of underperformance.

The good news about broadening your horizons to other high-quality companies is that you don’t need to dump all your tech stocks. There is a fair amount of overlap between big tech and quality (NVIDIA and Microsoft are the two largest holdings in the QUAL ETF), but the less or non-profitable AI related companies aren’t included.

We have always tilted strongly toward quality in our portfolios, but we are only trimming our NVIDIA, Microsoft and Broadcom positions, not selling them completely. However, their weights in our portfolios are far lower than in the S&P 500, and we also own stocks such as Costco, Procter & Gamble, Amgen and Fastenal (who doesn’t love screws and nuts!) which continue to grow and earn high profit margins.

As we have said many times before – there is no need for drastic action. Trimming back the more speculative parts of your portfolio and adding in some boring stuff (or even – perish the thought – some investment-grade bonds) should help mitigate some of the damage from another “flesh wound” that could occur at any time, for any reason.

The Fed Finally Cuts and the Government Shuts Down

We normally discuss the latest inflation report, but it won’t be released until late October, as there is nobody at the Bureau of Labor Statistics to write the report. This is a minor consequence of the federal government’s shutdown. While government shutdowns can worry a lot of people – particularly federal workers who aren’t getting paid (including some who must work without pay) – the country seems to handle them well over the long run, and the stock market rightfully treats this as the parent shaking their head at the squabbling children at the playground. There is a lot of noise and chaos, then everyone goes home and forgets it happened.

In other government (or quasi-government) news, the Fed finally cut rates! Did you feel the ground shake? Did you hear the trumpets playing and the angels singing? No? It was just another day? Well, the Fed did its job and made the cut very anticlimactic. The market hates surprises, and one of the primary jobs of Chairman Jerome Powell is to make the moves so clear and so far in advance that everyone shrugs their shoulders when it happens.

The market expects two more 25 basis point (0.25%) cuts in 2025, which will hopefully help lower rates on auto loans and mortgages – particularly mortgages, which have priced many people out of homeownership recently. However, the cuts continue even with inflation above the Fed’s “official” goal of 2%. Since the Fed has a “dual mandate” of low inflation and full employment, the seesaw is continuing to tip toward the “employment” mandate, as the unemployment rate gradually rises from what had been 40-year lows.

The cuts increase the risk of persistent inflation, but also please the politicians of both parties (although President Trump has been the most vocal about larger cuts, to the point where he was thinking of a way to fire Chairman Powell without freaking out the markets) since a strong economy gets people re-elected, and mid-term elections are one year away.

As usual, we prefer investors to stay above the noise, not chase trends or fads, avoid drastic moves based on news, and build a diversified portfolio that supports a solid financial plan. Enjoy the football games and changing leaves, and we will return in January for our year in review. Please contact us if you have any questions.