2025 Q4 Review and Outlook – Stocks Follow Profits

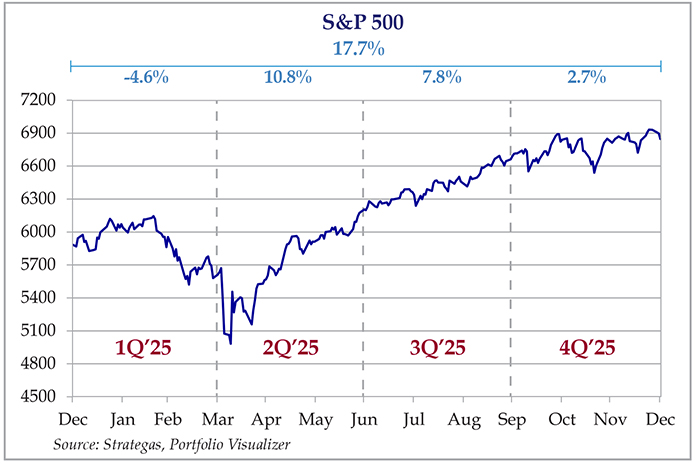

The market capped a strong year with a positive fourth quarter as stocks (as measured by the S&P 500 SPDR ETF – SPY) rose 2.7%. The U.S. bond market (as measured by the US Aggregate Bond ETF – AGG) gained 0.9%, and a 60% stock/40% bond portfolio earned a 2.0% total return. For the full year 2025 stocks gained 17.7%, bonds gained 7.2% and a 60/40 portfolio gained 13.5%. Looking further back, the past ten years’ returns were equally impressive, with stocks gaining 14.7% per year, bonds 1.95% and a 60/40 portfolio (rebalanced annually) 9.75%.

Figure 1: S&P 500 quarterly performance, trailing four quarters.

Stocks keep charging ahead – in line with profits

This is getting to be repetitive, but the stock market had yet another double-digit gain – the third year in a row of exceptional returns. We are very happy with the outcome, even though there is a tendency (especially in this decade’s increasingly toxic social media environment) to view any good financial news with skepticism or even fear. A lot of commentators love to use the baseball analogy, and we have been in the “7th, 8th or 9th inning” of economic expansion/bull market/etc. for about five years. And then there’s the whataboutisms. “What about the debt?” “What about the housing affordability?” “My second cousin just got laid off – this must be the first steps of a recession!” A financial pundit will find some obscure economic indicator that is going down and declare it “the canary in the coal mine!”

It’s enough to drive anyone crazy. People aren’t robots, and even the most calculated and analytical people are influenced by feelings and personal biases. One particularly relevant quote we spotted on social media says, “people don’t make decisions based on data – they make decisions based on their feelings about the issue and then find the data to support their decision after the fact.”

As professional investors, we must be doubly vigilant against biases and knee-jerk reactions, since a) we are paid to be as objective as possible, and b) our actions don’t just affect our financial lives, but the financial lives of many other people. Many of those people are just as smart as us and perfectly capable of managing their own portfolios, but have us manage it for them because they have the self-awareness to realize that they either a) aren’t psychologically or emotionally prepared for the process, or b) are quite level-headed, but don’t want the psychological burden taking up too much space in their heads. If you are running a business or managing a household which has 4-5 kids in various life stages or taking care of a spouse or parent with a chronic illness, the added decision-making burden can be just too much.

With that said, rather than be immediately skeptical of a three-year bull market (or a cheerleader screaming “this time is different!”), let’s look under the hood and see where we stand.

Profits have grown

The number one key driver for long-term stock price performance is growth in profits. For short-term periods, the stock price may make wild jumps and drops, but over multiple years, that random zig-zag stock price line will follow the general trend in profit growth. If a stock’s profits grow 10% per year for 20 years, the stock price plus reinvested dividends should grow 8%-12% per year. That 8%-12% per year will undoubtedly include several +30% years and -20% years along the way, but earnings are like a magnetic field which keeps pulling the stock price back to the general trend.

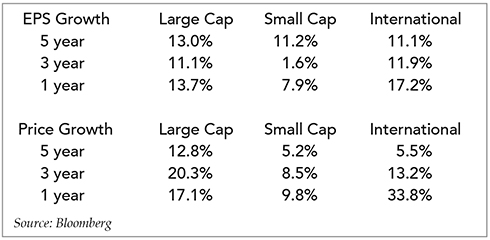

Based on the following tables, the stunning performance of the S&P 500 (large cap stocks) is largely due to impressive earnings per share (EPS) growth: 13% per year for the past 5 years. This exceeded both small cap and international stocks. Accordingly, investors flocked to the higher growth and the S&P 500 beat every other major index in terms of stock price growth.

Figure 2: Annualized EPS and stock price growth, Large Cap, Small Cap, International

This is not to say that we are guaranteed to continue at this rate for the next five years (despite what the AI evangelists are shouting) – only that the strong rally has, in aggregate, a rational basis. There are certainly profitless “meme stocks” that skyrocketed, but a lot of that comes out in the wash. For every meme stock up 1000%, there are little-mentioned stocks that went to zero.

Another interesting trend is the sharp increase in international EPS growth over the past year (which also explains the outperformance vs U.S. stocks in 2025). International stocks have lagged U.S. for over a decade. Could this long term trend reverse to produce an international decade of outperformance? That is beyond the range of our crystal ball (which never seems to work anyway) but it certainly is something to pay attention to.

Valuations favor small and international

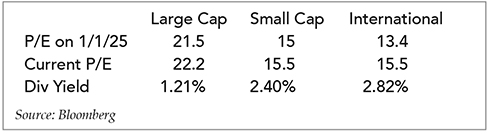

The other major piece of the puzzle to future returns is valuation. How much money are you paying for every dollar of profits? If expectations are high, then investors are willing to pay a premium for stocks as they expect the growth trend to continue (and vice versa). As Figure 3 illustrates, large cap U.S. stocks are trading at a premium to small and international stocks, which implies higher future EPS growth. Small and international stocks are also expected to pay higher dividends.

Figure 3: Valuation of Large Cap, Small Cap, International

This seems cut and dried. International and small cap EPS growth has caught up to U.S. large cap and the stocks are cheaper. Easy decision! As Lee Corso always said on ESPN’s College Game Day – “Not so fast my friend!” Large cap stocks have been more expensive than small and international for almost the entire duration of its decade-long outperformance. They just kept riding the wave of profit growth, with some brief crashes in 2020 and 2022 (what happened in 2020 again? Our memory is kind of fuzzy.)

So it’s really a matter of the AI and/or technological growth continuing to support “big tech” to maintain the relatively high expectations set by the S&P 500’s valuation. And it’s not a bad bet – investor money continues to pour into AI companies and datacenters (which are filled with processors and memory chips). However, there are many unpredictable events that may upset this high-tech apple cart, and the consequences to tech stocks’ stock prices would be severe. International growth seems to be holding up – especially given the chaotic geopolitical environment – with increased defense spending and a slight tilt towards more capitalist-friendly policies in certain countries.

What we do in this situation is simply to own a little bit of everything and make what we own as high quality as possible. Like elite athletes, high-quality companies tend to find themselves in the right place at the right time and also bounce back from inevitable setbacks more quickly than low-quality companies. We did push our allocation to international stocks a bit higher at the beginning of the year, but this was a carefully measured step, not a knee-jerk reaction to the news. Diversification solves a lot of investment problems. But that’s boring and won’t get anyone rich quickly, so you don’t hear about it on social media or especially CNBC.

The 2025 Winners (and some losers) – tech, tech and more tech

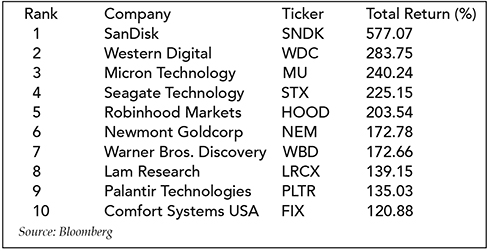

At the end of every year, it’s interesting to look back at the winners and losers of the previous year. While the S&P 500 grew over 17% in 2025 (which is amazingly good), it is made up of about 500 stocks, most of which had either much better or much worse returns than the index. Figure 4 shows the top 10 S&P 500 stocks for 2025 in terms of total return (stock price plus reinvested dividends) and there were some whoppers in there.

Figure 4: Top 10 S&P 500 stocks, 2025 total return

This is a very tech-heavy list. The top four stocks make components for computer memory (SanDisk – flash memory, Western Digital and Seagate – disk drives, Micron – memory chips). These are all going into data centers. Robinhood is the hot place for the kids to trade tech stocks and cryptocurrencies. As an “old media” company, Warner Brothers probably wouldn’t have been on the list had it not been the subject of a bidding war between Netflix and Paramount (who just want the intellectual property and will probably gut the rest). Gold has been on a tear and Newmont is one of the largest gold miners in the world. Lam Research and Palantir are both huge tech stocks (and Palantir is probably watching you read this newsletter – say hi!) Comfort Systems is an “old economy” industrial company that just happens to make a lot of HVAC systems needed to run data centers and microchip factories.

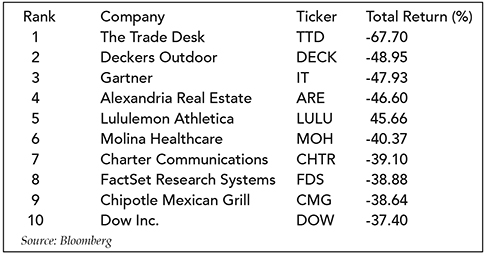

The bottom 10 is more of a mixed bag, with a surprising number of name-brand, “quality” companies. The Trade Desk was a super-hot tech stock that fell back to earth. Branded apparel companies such as Lululemon and Deckers (maker of UGG boots) have suffered under tough competition and high tariffs which squeezed margins (Nike also had an awful year, down almost 14%). Gartner is a tech consulting company that is threatened by AI. Alexandria Real Estate is a REIT that specializes in biotech labs, and biotech didn’t have a good year. Molina Healthcare was caught up in the managed care meltdown which had larger competitor UnitedHealth Group in the news. Charter Communications is a cable TV company in a “cord-cutting” era with a lot of debt. Dow is a highly cyclical chemical company on the wrong side of the cycle. Factset and Chipotle are still growing, but they had sky-high expectations coming into 2025 and were punished severely when growth slowed down unexpectedly.

Figure 5: Bottom 10 S&P 500 stocks, 2025 total return

Growth and/or momentum investors will be picking through the winners to see which ones to continue to ride, while old-school value investors will be picking through the losers for “scratch and dent specials” that may have overreacted. We are somewhere in the middle. We just try to find the best businesses with strong market positions and try to buy them at decent prices. These are very hard to find, so we don’t make a lot of changes in a given year. Most investors are served well enough to stay out of the stock-picking game and diversifying across several asset classes. Remember that your buddy at the country club who brags about his big winners will rarely mention his losers.

The Economy Keeps Chugging Along

Now that government agencies are back at work, economic data is gushing back into the news stream, and most of it is “good but not too good.” The latest inflation numbers were comfortably below 3% (headline CPI grew 2.7% year over year and Core CPI 2.6%) despite continued upward pressure from tariffs and housing prices. The latest jobs report showed a slowing but still positive increase in payrolls and a 4.4% unemployment rate, which remains very low by historical standards.

These “good but not great” numbers were music to investors’ ears, because it opens the door just wide enough for continued interest rate cuts by the Fed. Lower interest rates generally lead to more economic activity, and we have already seen a modest but very welcome drop in mortgage rates, which instantly improves home affordability. Futures prices currently anticipate two 0.25% rate cuts in 2026, which could maintain or even boost economic growth – at the risk of a return to higher inflation.

This tug of war over rate cuts has come to a head recently, with President Trump playing hardball with Fed Chairman Jerome Powell, including a Justice Department investigation into the cost of the Federal Reserve Building renovations. This year is mid-term elections (standby for more political ads and robocalls!) and President Trump needs a red Congress to maintain his near carte blanche regarding political decisions (including the recent military operation in Venezuela, demands to take over Greenland, capping credit card interest rates at 10%, and on and on and on…) He knows that, to quote James Carville, “It’s the economy, stupid!” when it comes to elections and wants the economy to run as hot as possible this year. Chairman Powell is out in May, and Trump’s next appointee will most likely be much more compliant with his wishes for lower rates.

With all that said, the big catalysts (positive or negative) usually come out of nowhere. Markets are so good at absorbing information that whatever is in the news is usually in the stock price. For that reason, we continue to ask investors to stay above the noise, not chase trends or fads, avoid drastic moves based on news, and build a diversified portfolio that supports a solid financial plan. Break out the wool socks and hot chocolate and we will check back in when the flowers bloom in April. Please contact us if you have any questions.