2025 Q2 Review and Outlook – Being Right vs. Making Money

The market staged a strong recovery in the second quarter of 2025 as stocks (as measured by the S&P 500 SPDR ETF – SPY) rose 10.8%. The U.S. bond market (as measured by the US Aggregate Bond ETF – AGG) gained 0.9%, and a 60% stock/40% bond portfolio earned a 6.8% total return. Year to Date (YTD), stocks gained 6.1%, bonds gained 3.7% and a 60/40 portfolio gained 5.1%

Figure 1: S&P 500 quarterly performance, trailing four quarters.

Being right vs. making money

Although this is beginning to sound repetitive, the second quarter was one of the most “interesting” quarters we have experienced in a while. The end of Q1 saw a buildup of tension regarding the impending tariffs, and that tension was released in early April, creating an extremely chaotic market as the news seemed to change every day (with the pundits sending out increasingly dire messages). However, just as the social media channels were set to melt down their servers, there was a huge reversal as some tariffs were delayed, and others rolled back. (You can see the “V” shape on the stock chart from orbit.) And now we are back at all-time high levels on the major indices such as the S&P 500 and the Dow Jones Industrial Average (DJIA).

Somewhere in the middle of all that, we bombed Iran.

The second quarter provides a perfect laboratory of investor behavior which imparts valuable lessons for investors. If you had followed the financial news and analyzed every nuance of the tariffs and made what you thought were the “right” investment decisions, you would have been completely whipsawed.

There’s a term traders and investors used to say – “do you want to be ‘right’, or do you want to make money?” That doesn’t mean that it’s bad to be “right,” or that you need to be “wrong” to make money. It’s about being right about the important things, and, more importantly, putting yourself in a position where you don’t have to be right over, and over, and over again. No one is perfect, and most people vastly overestimate their ability to make the correct short-term decisions (especially under pressure). However, just making a few key long-term decisions makes everything so much easier.

Being “right” stems from a desire for control. Many successful people (who now have millions of dollars to invest) became successful by maintaining control of their business or their career and being right about a lot of things. They also have huge work ethics and understand that “the harder you work, the richer you get.” Unfortunately, this desire for control and “trying harder” can massively backfire in investing, because trying to think faster than the market in the short term can leave you turned around and upside down very quickly.

What about us? We closely follow the financial news and markets. We work hard. We buy and sell individual stocks. Aren’t we just trying to be “right?” Well, yes and no. Of course we must make good decisions about what to include in our portfolios. We like to buy stocks that go up. However, we own a lot of different stocks, because we also know that we aren’t perfect. We have been and will continue to be “wrong.” But, no one stock (or mutual fund or ETF) will materially move the portfolio. Also, we take a relatively long-term view and try to stay out of the noise. We look for stocks that will be significantly more valuable in 5-10 years, not 6 months. And finally, this is our job. We do this 8 hours a day, 5 days a week (and sometimes on weekends for fun).

A great example is NVIDIA (NVDA). We bought NVDA during the chaos in early April after it fell from $150/share to just under $100. It is now trading at over $170/share. If we were less scrupulous, we would have shouted this from the mountaintops and built an entire marketing strategy around this decision. But we didn’t, because a) it was simply one decision out of many we have to make every year; b) NVDA is only targeted to 3.3% of our individual stock portfolio (2.4% if you include the other equity funds and ETFs); c) we really won’t know if we are “right” for at least three if not five or ten more years; and d) we would also need to compare this to all of our “wrong” stocks (which are fewer than the “rights” but definitely not zero.) Also, this wasn’t a knee-jerk reaction – we have been watching this stock for several years, building up enough knowledge to be able to pull the trigger when the opportunity presented itself.

So how do you bypass these very human instincts that sabotage financial success? Probably the best way to approach an overall investing strategy is to a) do the hard work up front by figuring out an overall asset allocation that matches your financial plan; and b) don’t make big changes to the portfolio because you think stocks are going to go up or down or that interest rates are rising or falling – make that big change because your overall financial picture has changed:

- Impending retirement/early retirement

- A large inheritance

- Buying a house/downsizing the house

- Job loss/job promotion/new job

- Marriage/divorce

Note that “Trump’s tweets” are not on that list, nor are “hot stock tips at the golf outing.”

If you still have that urge to be “right,” then carve out a small percentage of your portfolio, put it in a Schwab or Fidelity or Robinhood brokerage account and treat it like the game that it is. Your own private casino. You may do quite well for a year or even several years, but you may find that “working harder” just spins your wheels faster in the mud.

The Big Beautiful Bill Passes

Speaking of personal financial events, the so-called “Big Beautiful Bill” won a very hard-fought battle and finally passed both houses. The stock market reacted positively, for two reasons: a) the bill is highly stimulative, with tax cut extensions and new deductions; and b) it passed! Remember that stock investors are skittish and don’t like uncertainty. Whatever you think of the bill (which does have some potential risks regarding the budget deficit and also cuts many programs to lower economic groups) it is done, and we can now make the necessary adjustments and get on with life.

Of course, from an investing standpoint, that’s in the rearview mirror. What is more important to 99% of our readers is the specific parts of the bill, which include:

- Permanent extension of earlier tax cuts

- Permanent increase to the estate/gift tax exclusion to $15 million per person (with an inflation adjustment)

- Increases the standard deduction for married filers to $31,500 (also with future inflation adjustments).

- Increase the State and Local Tax (SALT) deduction to $40,000 (which will phase out in 2029 if not extended)

- Deductions for tips and overtime income.

There are many more provisions, and almost all of them represent lower taxes (unless you buy an electric car), and could put more money in your pocket than any stock trade you could dream up (because those stocks probably went up before the bill was passed). Again, we have concerns about the impact to the deficit and national debt (which is one reason why President Trump is putting so much pressure on Fed Chairman Jerome Powell to lower interest rates). But for the time being, it’s mostly good news.

International is the star of 2025 (so far)

In other investing news, the prodigal son has returned! Despite the headlines about NVIDIA and other U.S. stocks, international stocks have actually outperformed their U.S. brethren in 2025 – by a wide margin.

International stocks (as measured by the Vanguard Total International Stock ETF – VXUS) had a YTD total return of over 18% to June 30th, compared with the S&P 500’s 6% return. This took everybody by surprise, since international stock returns have lagged U.S. stocks for the past 15 years. There are many reasons why we think this has happened – a weakening dollar, lower interest rates and more industrial development in Europe, a more shareholder-friendly Japan, etc. However, rather than dwelling on the causes or speculating on the sustainability of this outperformance, we simply use it as an example of the benefits of diversification. We have always had an allocation to international stocks, and it has been painful at times.

While our international weighting is lower than our benchmark it is still enough to matter at 14% of our stock portfolio. We may increase it, decrease it, or keep it at the current level, but we aren’t going to make any changes based on 6 months of data. However, we will most likely continue to have an allocation, because sometimes, when U.S. stocks “zig,” international stocks “zag,” and that can help smooth out long-term investment returns.

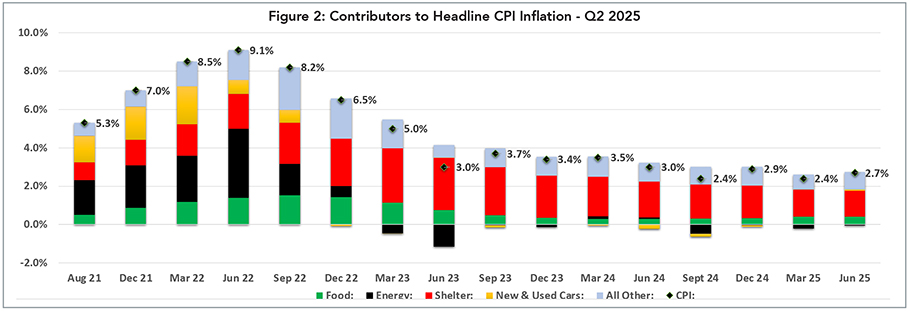

Inflation – Steady, but signs of tariffs in the water

The latest inflation report was steady, but still above the Federal Reserve’s 2.0% goal. As Figure 2 shows below, the CPI index bounced to 2.7% year over year growth from 2.4% at the end of last quarter. Furthermore, the more stable “Core” (i.e., minus food and energy) inflation ticked up to 2.9% from 2.8%, which ended a multi-year downward trend. Shelter inflation continues to be stubborn, but car price inflation was very low. Energy prices were slightly down, which repeated the last quarter’s results.

This puts the Federal Reserve in a bit of a pinch, as the Board of Governors (and particularly Chairman Jerome Powell) has adopted a very cautious approach to rate cuts – particularly in the wake of the theoretically inflationary tariff policies. However, the economy is not exactly rocketing upward, with job growth and industrial production softening (not to mention the stagnant homebuilding industry, which is highly interest rate sensitive). Chairman Powell has also found himself on President Trump’s naughty list, with Mr. Trump openly calling for his resignation if he isn’t willing to lower rates aggressively. These comments have spooked investors, which is why Trump hasn’t simply fired him.

In a way, we can understand Mr. Powell’s dilemma (pressure from the White House notwithstanding). Go too slow on rate cuts, we may tip into a recession or even “stagflation” if the tariffs’ effect on prices hit worst case scenarios. On the other hand, cutting rates into the teeth of another inflationary cycle threatens us with a repeat of the post-COVID inflationary boom, which is also something no one wants to repeat.

Right now, most forecasters project the fed funds rate to be about 50 basis points (0.50%) lower by January 2026, which implies two 25 basis point cuts. To the extent that the actual cuts deviate from these expectations, the short-term market volatility could increase.

Source: Bureau of Labor Statistics

Source: Bureau of Labor Statistics

Of course, for people with a 20-40 year investment horizon (which is probably 95% of the investing public), short-term volatility is noise that pales in comparison to a properly constructed financial plan paired with an appropriate asset allocation. Once you have those two dialed in, CNBC becomes a source of entertainment rather than something to take seriously. (Jim Cramer is pretty funny.) Try to stay cool in the Summer heat and we will return with our 3Q review as the leaves start to turn. Please contact us if you have any questions.